Ever paid $10 for your blood pressure med and thought, "At least this is getting me closer to my deductible"? You’re not alone. Millions of people assume that every copay they make-whether for a doctor visit or a generic pill-counts toward their deductible. But here’s the truth: generic copays usually don’t count toward your deductible. They do count toward your out-of-pocket maximum. And that difference can cost you thousands if you don’t understand it.

What’s the difference between a deductible and an out-of-pocket maximum?

Your deductible is the amount you pay for covered services before your insurance starts sharing the cost. For example, if your plan has a $2,000 deductible, you pay the first $2,000 of medical bills yourself. After that, you might pay 20% coinsurance while your insurer pays 80%.

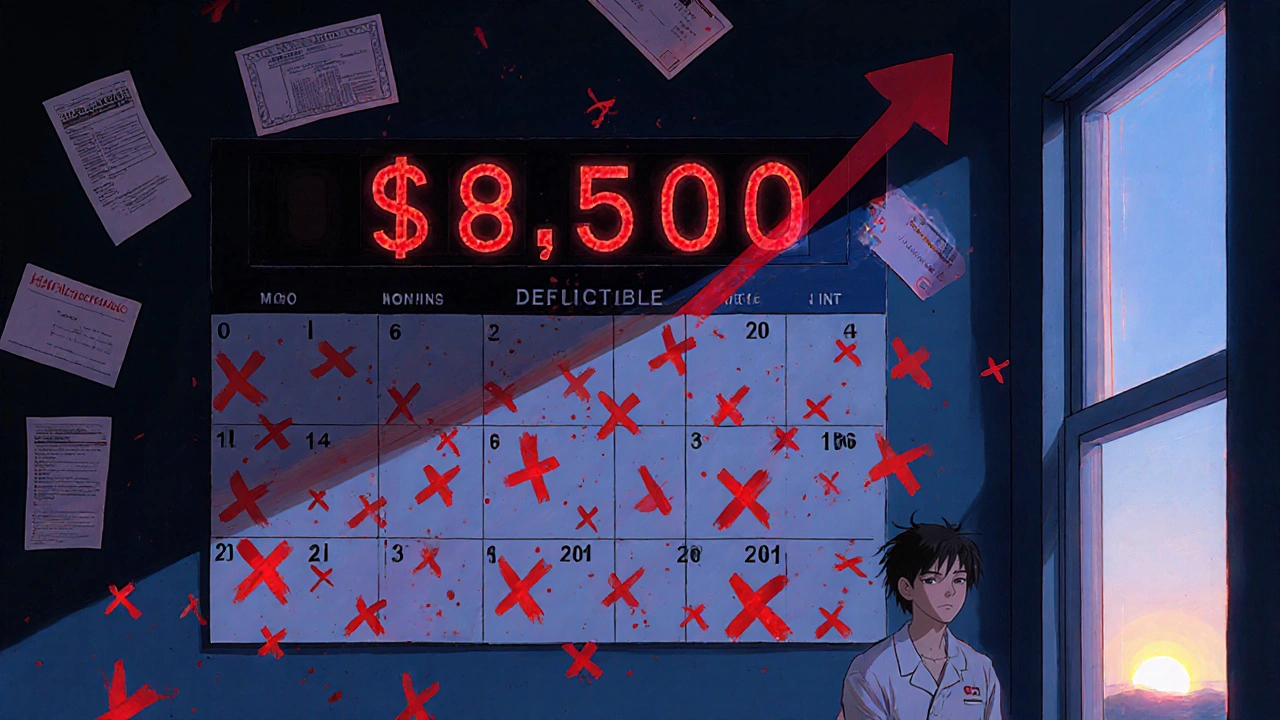

Your out-of-pocket maximum is the most you’ll pay in a year for covered care. Once you hit that limit-no matter what kind of costs you’ve paid-your insurance covers 100% of everything else for the rest of the year. In 2025, the max for an individual is $9,200. For families, it’s $18,400.

Here’s the key: all your in-network costs-deductibles, coinsurance, and copays-add up to your out-of-pocket maximum. But only some of them count toward your deductible. And generic prescription copays? They almost never do.

Why don’t generic copays count toward your deductible?

This setup wasn’t always the case. Before the Affordable Care Act (ACA) took full effect in 2014, many plans didn’t count any copays toward anything. People with chronic conditions-like diabetes or high blood pressure-could pay $15 or $20 every month for their meds and still be nowhere near their deductible. They were stuck paying full price for everything else, even after spending hundreds or thousands on prescriptions.

The ACA fixed one big problem: it made sure all cost-sharing counts toward your out-of-pocket maximum. That means your $10 insulin copay? It adds up. If you’ve paid $8,500 in copays and coinsurance, you’re done paying for the year-even if you haven’t met your $2,000 deductible.

But the ACA didn’t merge deductibles and copays. Why? Because insurers and policymakers wanted to keep a financial "gatekeeper"-the deductible-to discourage unnecessary care. So now you’ve got two separate tracks:

- Deductible track: You pay full cost for services until you hit your deductible. Copays usually don’t move the needle here.

- Out-of-pocket maximum track: Every copay, coinsurance, and deductible payment adds up. Once you hit the max, you’re covered.

That’s why someone can pay $3,000 in generic copays over a year and still have a $0 deductible. They’re not "in the clear" for other care-they’re just done paying for everything else because they hit their out-of-pocket max.

How do different plan types handle prescription costs?

Not all plans work the same. There are three common structures:

- Single deductible: One amount covers both medical and prescription costs. If you have this, your generic copays do count toward your deductible. But only 27% of employer plans use this model.

- Separate medical and prescription deductibles: You have two deductibles-one for doctor visits, one for meds. You pay full price for prescriptions until you hit the prescription deductible. After that, you pay copays that count toward your out-of-pocket max but not your medical deductible. This is the most common model, used in 37% of plans.

- Copay-only (no prescription deductible): You pay a flat copay for prescriptions right away, no deductible to meet. But again, those copays don’t count toward your medical deductible. This applies to 36% of plans.

So if you’re on a plan with separate deductibles and you’ve been paying $10 for your asthma inhaler every month, you’re probably not getting any closer to your $1,500 medical deductible. But you are getting closer to your $8,500 out-of-pocket max.

Real stories: What happens when people get confused?

People are getting burned by this confusion every day.

One user on HealthCare.gov wrote: "I paid $10 copays for my blood pressure meds all year. I thought I’d met my $2,000 deductible. Turns out I hadn’t. I still had to pay full price for my MRI." She paid over $2,500 in copays and still owed thousands more.

On Reddit, another person said: "I thought my $15 copay for my cholesterol med was helping me get to my deductible. I didn’t realize my plan had a separate prescription deductible I hadn’t met. I ended up paying $400 for a single prescription because I didn’t know I was still in the deductible phase."

A 2023 survey found that 68% of consumers believe prescription copays count toward their deductible. Only 22% know the truth. That’s a massive gap-and it leads to people skipping meds, avoiding tests, or getting hit with surprise bills.

On the flip side, people with chronic conditions are grateful for the out-of-pocket max. One user on PatientsLikeMe shared: "Before 2014, my insulin copays didn’t count toward anything. Now, I hit my $8,500 max last year. My meds were free for the rest of the year. That saved me over $3,000."

How to find out how your plan works

You can’t guess. You have to check.

Every plan must give you a Summary of Benefits and Coverage (SBC) before you enroll. Look for this section:

- "Does this payment count toward my deductible?"

- "Does this payment count toward my out-of-pocket maximum?"

It’s usually in a table. If it says "No" next to "Deductible" but "Yes" next to "Out-of-Pocket Maximum" for prescriptions-you’ve got the common split structure.

Also look for the Explanation of Coverage document. It’s longer, but it spells out exactly how each cost works.

Don’t rely on your pharmacy’s app or your insurer’s website. They often simplify things. The SBC is the only document legally required to be clear and standardized.

What’s changing in 2025 and beyond?

The government is trying to fix the confusion. In April 2024, the Department of Health and Human Services announced new rules for 2025 plans: insurers must clearly label how prescription costs count toward deductibles and out-of-pocket maximums.

Some insurers are testing "integrated deductible" plans-where prescription costs, including copays, count toward one combined deductible. Early results show patients stick to their meds 28% more often.

McKinsey predicts that by 2027, 60% of major insurers will offer at least one plan where generic copays count toward the deductible. But the American Hospital Association warns: simplifying this could raise premiums by 3-5%. So it’s a trade-off: simpler rules might mean higher monthly payments.

For now, the system stays complicated. But knowing how it works? That’s power.

What you should do right now

Here’s your action plan:

- Find your plan’s Summary of Benefits and Coverage (SBC). If you can’t find it, call your insurer and ask for it.

- Look at the table for "Prescription Drugs." Check the "Deductible" and "Out-of-Pocket Maximum" columns.

- If copays say "No" for deductible but "Yes" for out-of-pocket max-you’re in the standard model. Don’t expect your meds to help you meet your deductible.

- Track your yearly spending. Add up all your copays, coinsurance, and deductible payments. When you hit your out-of-pocket max, call your insurer to confirm your benefits reset to 100% coverage.

- If you take multiple prescriptions, ask if your plan has a preferred pharmacy or mail-order option. Some plans offer lower copays for 90-day supplies.

Knowing this isn’t just about saving money. It’s about making sure you don’t skip a needed med because you think you’ve "paid enough." You might have paid a lot-but you’re still in the deductible phase. And that’s when you’re most vulnerable to surprise bills.

Out-of-pocket maximums were designed to protect you. But only if you understand how they work.

Do generic prescription copays count toward my deductible?

In most cases, no. Generic copays typically do not count toward your medical deductible. They count toward your out-of-pocket maximum instead. This is true for plans with separate medical and prescription deductibles (37% of plans) or copay-only prescription coverage (36% of plans). Only plans with a single combined deductible-used by 27% of employer plans-allow prescription copays to count toward the deductible.

Do copays count toward my out-of-pocket maximum?

Yes. All in-network cost-sharing-including generic prescription copays, coinsurance, and your deductible payments-counts toward your out-of-pocket maximum. This has been required by the Affordable Care Act since 2014. Once you reach your annual out-of-pocket maximum, your insurance pays 100% of covered services for the rest of the year.

Why do insurers separate deductibles from copays?

Insurers use separate deductibles to encourage more careful use of healthcare services. The deductible acts as a financial "gatekeeper"-you pay full price until you meet it, which discourages unnecessary visits or tests. Copays are meant to be a fixed, predictable cost after that point. Keeping them separate lets insurers control costs while still protecting consumers from catastrophic bills through the out-of-pocket maximum.

How do I know if my plan has a separate prescription deductible?

Check your plan’s Summary of Benefits and Coverage (SBC). Look for a section titled "Prescription Drugs" and find the row for "Deductible." If it says "Yes" under "Prescription Deductible" or lists a separate dollar amount for prescriptions (like $500 for meds vs. $1,500 for medical), you have a separate deductible. If it says "None" or "Not Applicable," you likely pay copays right away with no prescription deductible.

What should I do if I’m confused about my plan?

Call your insurance company and ask: "Do my generic prescription copays count toward my medical deductible? Do they count toward my out-of-pocket maximum?" Request a copy of your Summary of Benefits and Coverage if you don’t have it. You can also log in to your insurer’s website and search for "SBC" or "cost-sharing summary." Don’t rely on pharmacy apps or general website descriptions-they often simplify or misrepresent the rules.

Can I switch plans to make this simpler?

Yes, during open enrollment (usually November-December) or if you have a qualifying life event. Look for plans labeled as having a "single deductible" or "integrated deductible." These combine medical and prescription costs into one deductible. While these plans may have slightly higher premiums, they eliminate the confusion and help you reach your out-of-pocket maximum faster if you take regular medications.

Julia Strothers

November 21, 2025 at 10:14So let me get this straight - the government forced insurers to count copays toward out-of-pocket maxes but NOT deductibles? Classic. This isn’t healthcare policy, it’s a psychological trap. They want you to think you’re ‘progressing’ while quietly draining your bank account. Next thing you know, they’ll start counting your coffee purchases toward your ‘mental health deductible.’ Wake up, people. This is designed to keep you confused and compliant.

Erika Sta. Maria

November 22, 2025 at 03:25wait but if copays dont count to deducible then why do they even call it a copay?? its like calling a banana an orange and then saying ‘oh but its not actually orange’ lol. this system is a joke. someone in a boardroom in new york probably got a bonus for this. also i think my cat has better insurance than me. 🐱

Nikhil Purohit

November 22, 2025 at 10:55Hey, this is actually super helpful. I’ve been paying $12 for my asthma inhaler every month and assumed I was inching toward my deductible. Turns out I’ve been on a separate prescription deductible I didn’t even know existed. Just checked my SBC - yep, ‘No’ under deductible, ‘Yes’ under out-of-pocket max. Gonna call my insurer today to confirm my max hasn’t been hit yet. Thanks for the clarity - this could’ve cost me big time.

Debanjan Banerjee

November 24, 2025 at 10:46There’s a critical nuance missing here: the distinction between ‘counting toward’ and ‘applying to.’ Copays count toward the out-of-pocket maximum by regulatory requirement under ACA Section 1302, but they are explicitly excluded from deductible accumulation under IRS guidance for qualified high-deductible health plans (QHDHPs). This isn’t an oversight - it’s intentional design to preserve the deductible’s function as a utilization gatekeeper. The 2025 HHS rule changes are a step toward transparency, but structural complexity persists because of actuarial risk pooling models that require segmented cost-sharing. If you’re on a separate prescription deductible plan, your copays are not ‘wasted’ - they’re simply allocated to a different financial bucket. Track both buckets separately.

Steve Harris

November 25, 2025 at 04:15Thank you for writing this. I’ve seen so many people panic when they get hit with a surprise bill after thinking their meds ‘counted.’ I work with patients every day and this exact confusion comes up weekly. The key takeaway? Don’t guess. Get the SBC. Print it. Highlight the prescription section. If your insurer won’t send it, file a complaint - they’re legally required to provide it. And if you’re on meds long-term, ask about mail-order 90-day fills. That’s often where the real savings are.

Michael Marrale

November 25, 2025 at 17:14Did you know the insurance companies lobbied to keep this system? They’ve been doing this since the 90s. The whole ‘out-of-pocket max’ thing? A PR stunt to make you feel safe while they still profit from your confusion. And the SBC? It’s written in 11-point font with invisible watermarks. They don’t want you to understand. They want you to pay. And if you do? They get to say ‘you signed the paperwork.’ I’ve got documents. I’ve got emails. This isn’t incompetence - it’s exploitation.

Elaina Cronin

November 26, 2025 at 14:05While the technical distinctions are well-documented, the emotional toll on patients cannot be overstated. I have worked in clinical ethics for over a decade, and I have seen patients forego necessary diagnostics because they believed they had ‘met their deductible’ - only to be presented with a $4,000 bill. This is not merely a policy flaw; it is a failure of fiduciary duty. The language used in insurance communications must be held to the same standard as medical consent forms: clear, unambiguous, and patient-centered. Anything less is unethical.

Willie Doherty

November 26, 2025 at 20:42Interesting. The ACA’s out-of-pocket cap was a necessary intervention, but the retention of the deductible as a separate construct reveals a deeper structural tension: consumer protection versus provider cost control. The fact that 68% of consumers misunderstand this suggests the communication infrastructure is broken, not the policy. The 2025 labeling mandate is a bandage. What’s needed is a unified cost-sharing model - but that would require insurers to relinquish revenue control. Unlikely. Meanwhile, we’re all just guessing.

Darragh McNulty

November 27, 2025 at 14:22THIS. 😭 I just hit my out-of-pocket max last month after 11 months of $15 insulin copays. My doctor said I was ‘close’ to my deductible - I believed her. Turned out I was at $8,400 out-of-pocket but $0 toward deductible. My next MRI was free. I cried. Thank you for making this so clear. I’m sharing this with everyone I know. 🙏❤️

Cooper Long

November 29, 2025 at 03:50Simple truth. Copays for generics don't count toward deductible. They count toward out-of-pocket max. That's it. Stop overcomplicating. Check your SBC. Call your insurer. Know your numbers. No drama needed. Just do the work.

Sheldon Bazinga

November 30, 2025 at 14:09bro i just found out my ‘$10 copay’ for my zoloft is actually just a tax on being mentally ill. the system is rigged. why do i have to pay for my meds like they’re a luxury? i’m not buying a new iphone here. also why does my insurance company have a CEO who makes 8 million a year? this is literally capitalism with a stethoscope. #medsnotluxury #insuranceisaripoff